Sponsored Content

David Gorman, of Team Asset Management, offers this week’s market review

RISHI Sunak, the UK Prime Minister, has surprised all but his own cabinet by announcing an early general election on 4 July.

Most pundits had favoured October or November this year, but the party conference season and the US presidential election seem to have scuppered those times. It also has more to do with recent positive economic news on inflation (headline rate down to 2.3%) and growth doing what was least expected and keeping Nigel Farage and the Reform party off guard.

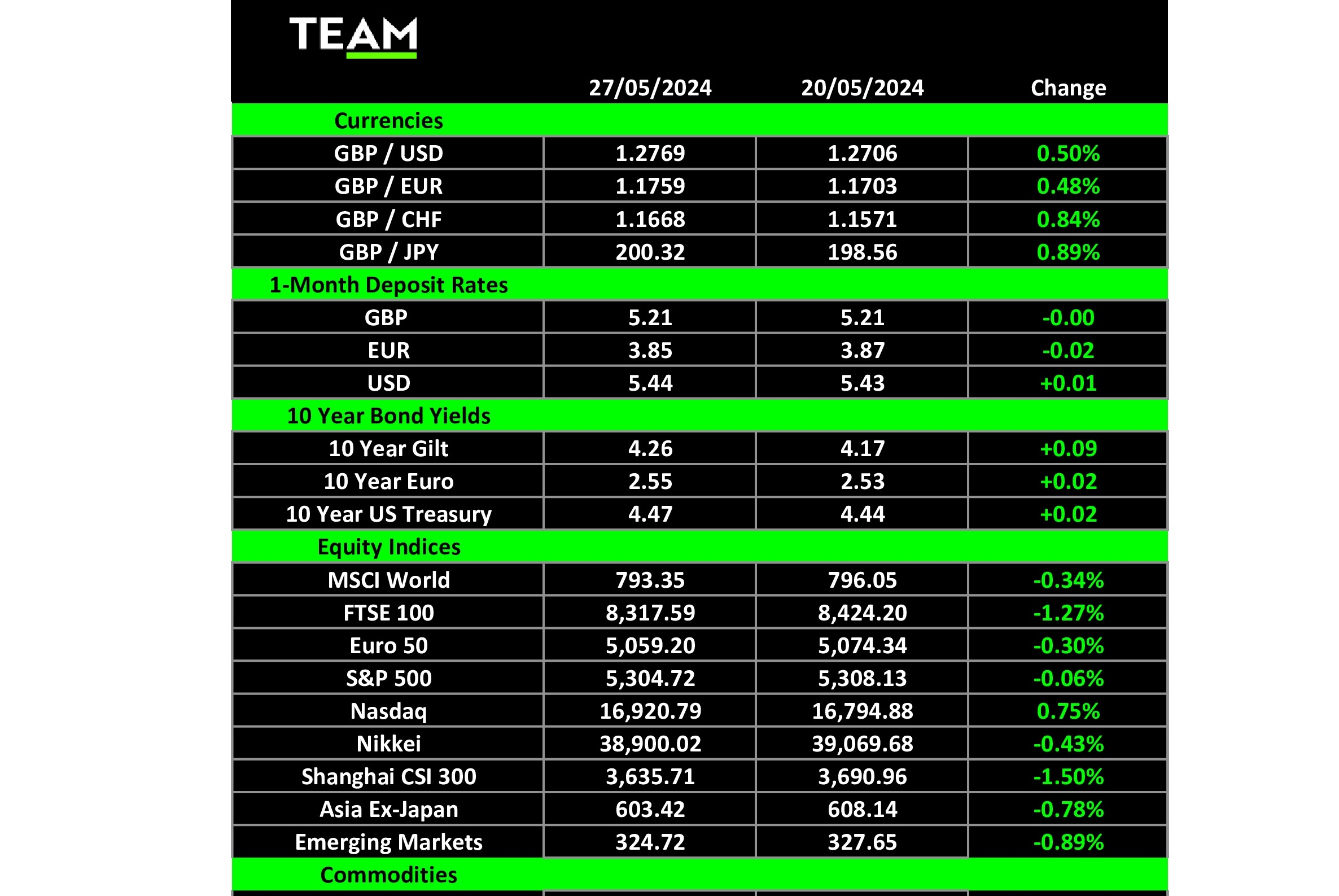

The UK and world markets moved down a little over the week, as stronger-than-expected US economic data pushed back the expected timing of interest-rates cuts by the Federal Reserve to later on in the year.

Only the technology-dominated Nasdaq index was able to push ahead to record levels following excellent corporate results. In fixed interest markets, yields rose modestly, given the underlying strength of consumer confidence and leading economic indicators.

The all-important US first-quarter corporate earnings results scorecard gives us a particularly good reason for equity markets to have done so well this year.

With all but a few companies yet to report, the aggregate S&P500 earnings increased by 6%, compared to the expected 3.4%, and more than three-quarters of companies beat consensus analyst forecasts.

Prime among these was artificial-intelligence star Nvidia, where demand for its data centre products sent first-quarter revenue to a staggering $26bn and year-on-year profits up by over 600%.

The shares broke the $1,000 level and have now gone up by 120% since the start of 2024.

National Grid, the UK power utility, confounded investors with a huge £6.8bn rights issue, the largest fundraising in 15 years in the UK, to upgrade its electricity networks. The shares predictably fell more than 10% following the announcement on Thursday but the five-year, £60bn infrastructure investment plan is likely to prove sensible and needed to maintain and improve network power reliability.

British financial services group Hargreaves Lansdown rejected a £4.7bn bid from a consortium that included private equity firm CVC Advisers and the Abu Dhabi Investment Authority. Its shares rose 22% and its main shareholder and founder, Peter Hargreaves, said that he was “watching with interest”. The board revealed that it turned down the 985p per share offer on the basis that it substantially undervalued the business.

For “crypto” followers, on Thursday the US Securities and Exchange Commission gave the go-ahead for the launch of Ethereum Spot Exchange Traded Fund. While there are further hurdles to overcome, it seems only a matter of time before Ethereum joins its big brother, Bitcoin Spot ETF, which launched on 11 January this year. Ethereum gained more than 11% on the week.

This week, investors should keep their eyes peeled on three events. First, Eurozone inflation data will be announced on Friday morning, while the US Federal Reserve’s preferred inflation measure will be released later in the day.

Finally, Donald Trump’s trial is concluding, with final arguments having taken place, which leaves the jury deliberations commencing with a decision possible by the end of the week. This could prove important given how close the polls are between Biden and Trump for the November election.