ARE central banks poised to cut interest rates? And is the world in a financial bubble?

These two questions formed the basis of Oakglen Wealth’s Spring Update, which, in the words of the company’s chief investment officer, Jeff Brummette, aimed to address “two topics that are big right now in the financial media”.

Responding to the first question, Mr Brummette, who was in the Island last week to deliver a series of presentations, said that “central banks were hinting at cuts and the market was trying to price such an event”.

“The one thing that really caught markets and a lot of investors off guard after Covid was that interest rates didn’t stay at zero or 1%,” he said. “At that point, a lot of people had significant exposure to fixed-income products, owning bonds that yielded little, if any, return. Sometimes they were losing people money.

“While no one could have predicted Covid, or the government response to it, once we started exiting the pandemic and inflation started to rise, there was an immediate sense that interest rates couldn’t stay down and that it was therefore necessary to move away from fixed income.

“Now, though, you can hold high-quality fixed income, with medium maturities of five to ten years, knowing that, almost no matter what happens, you won’t lose money because, even if something bad happens to the stockmarkets, those bonds will perform unless there is a repeat of 2022 and central banks raise interest rates again, something which doesn’t seem likely.”

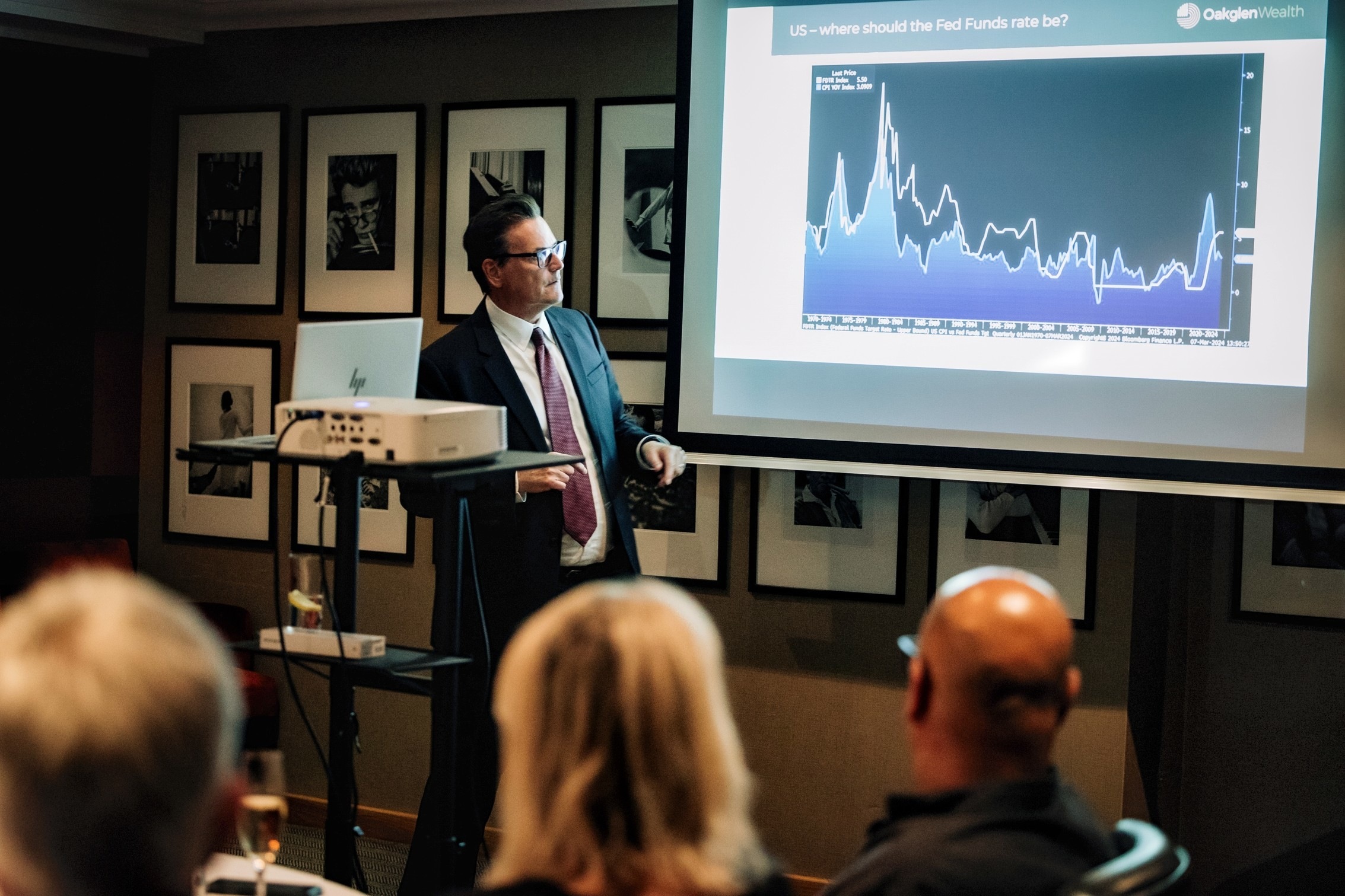

Indeed, with inflation “as under control as we have seen it in the past two years”, Mr Brummette said there was “every indication” that rates could be lowered.

“This is dependent on the data but if inflation stays as it is and the labour markets soften a touch – something which the Federal Reserve would argue is happening – then rates will fall slightly,” he said. “I think it will be a modest readjustment of rates, with the Fed perhaps cutting them from 5.25% to 4.5% over six to 12 months.”

Whether such cuts are necessary is, he suggests, “another story”.

“The markets have already started the year strongly, particularly among some of the technology sectors in America, so, while cuts may fuel further strength, they may not be needed,” he said. “We don’t really see anything exogenous or on the macro front which is likely to derail economic activity or equity markets.”

That remark was, however, tempered with a quick nod to the impending elections this year, particularly those in the UK and the US.

“We know that the US election will be a repeat of the 2020 [Donald] Trump versus [Joe] Biden contest,” said Mr Brummette. “Biden has passed two bills – the inappropriately named Inflation Reduction Act and the CHIPS Act – which are designed to stimulate the use of sustainable energy and the creation of chip-building factories, respectively. However, while both of these are good ambitions, if people are only buying electric vehicles because the government is subsidising them, that may hint at underlying weaknesses. Meanwhile, Biden is clearly slowing down and voters have to weigh up whether he can serve another term.

“The flipside is that Trump is very narcissistic and, while he says that he is supportive of America, some of the things he’s talking about – such as a 60% tariff on imported goods – are pretty radical. Then his treatment of the country’s allies, almost encouraging Putin to attack countries which don’t spend more on defence, is ridiculous and reckless. The danger of Trump as president is that he doesn’t necessarily have America’s best interests at heart or have much of an attention span or focus on details.”

With the election result therefore uncertain, Mr Brummette advises investors to “prepare for some volatility and make sure you have a portfolio that is diversified enough that you are not exposed to some radical policy that a new government may try and impose”.

Despite this potential uncertainty, Mr Brummette says that, financially, the world “feels more stable than it has done for the past couple of years”.

“The financial markets have now adjusted and, while real estate hasn’t fully adjusted, the overall situation feels more settled,” he said. “However, lurking in the background is the fact that many countries now have enormous fiscal deficits – the US fiscal deficit is becoming a bigger line item than defence spending, which was $895bn in the latest Biden budget – and with interest rates now at normal levels, debt-servicing costs are much higher than they were during the great financial crisis when central banks bought significant levels of debt issuance each year as part of their quantitative easing policies. This will become an issue at some point; it is just hard to say when.”